Who would win the Platypus War? Vector ($VTX) or Echidna ($ECD)?

Deep Dive into the tokenomics of Echidna Finance and Vector Finance

Both positioned as the “Convex Finance” designed for Platypus Finance, yield optimizer platforms Vector Finance ($VTX) and Echidna Finance ($ECD) were launched yesterday both on TraderJoe. The two platform come hand in hand and share similar vision - to maximize yield for liquidity providers on Platypus Finance. It seems that a Platypus War is about to commence, but which protocol is going to be the platform that rules?

What is Platypus Finance ($PTP)?

Platypus Finance establishes itself as one of the best stableswap platforms on Avalanche shortly upon its launch last December. With the Asset Liability Model which enables single-sided liquidity provision, the protocol solves problems like price slippage and impermanent loss that had been bothering users of first-generation decentralized exchanges.

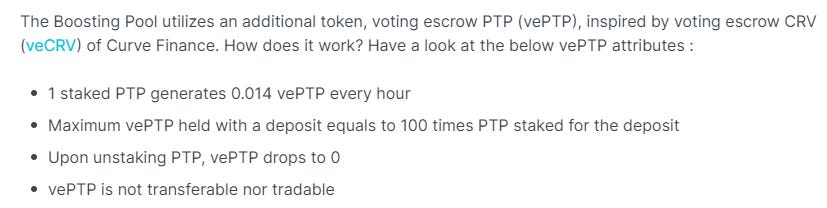

Stablecoin liquidity providers are rewarded with its native token $PTP and by staking it, they could boost their reward APY to over 100% - though there’s a twist here. It takes 10 months (i.e. ~7142 hours by simple calculation of 100 divided by 0.014) for users to maximize their yields - and unstaking of any amount of $PTP reduces vePTP to zero immediately.

The special tokenomics designs suppresses mercenary capital from selling $PTP for profit after accumulation, but also creates a user experience loophole to be plugged. That is why Vector Finance and Echidna comes into play.

Which protocol has the odds of winning the Platypus War?

Convex was deemed as the “winner” of the Curve Wars as the protocol has the most $CRV locked in their ecosystem. Therefore, let’s also establish that whichever protocol is able to lock in the most $PTP would be the winner of the Platypus War - and the key to attract the largest amount of $PTP is the reward.

Both platform serves the two subsets of users in the market related to Platypus - $PTP holders and liquidity providers of stablecoins on Platypus. Let’s discuss one by one.

Firstly for the $PTP holders, both protocols enable staking of Platypus’ native token $PTP to yield rewards. For Echidna, $PTP is turned into $ECD upon staking and with a 2 year lock-up period of $ECD would it reward users with 5% to 10% of protocol’s revenue in $PTP and voting rights on both Echidna Finance and Platypus Finance.

Vector works in a similar way which upon staking of the minted xPTP would users be entitled to 71% of the protocol’s revenue in $PTP and its native governance token $VTX as extra reward. By staking $VTX, users would receive the remaining 29% revenue of the protocol.

In comparison, Echidna Finance pays a smaller cut of the protocol’s revenue to $PTP holders but rewards them by a governance token that is supposed to have more stable price thanks to the two-year locking period. Vector Finance rewards $PTP holders with a lucrative 71% protocol revenue while its governance tokens might face selling pressure from mercenary capital.

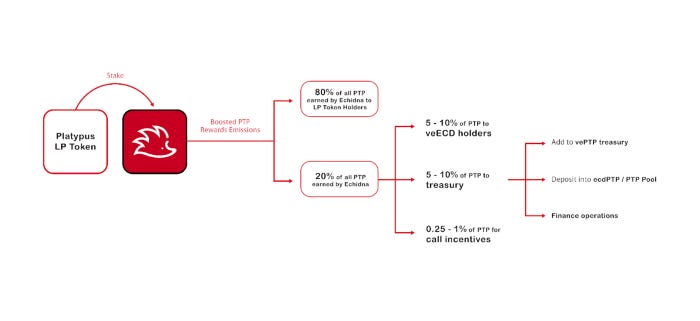

For the second subset of target audience - stablecoin liquidity providers, Echidna Finance rewards them with the boosted $PTP rewards and 80% of it would go to LP tokens holders, while 20% would be earned by Echidna Finance. Whereas for Vector Finance, rewards would be in the form of $VTX and the boosted $PTP.

So…what does the difference in tokenomics and reward mechanism tell us?

Platypus Finance is designed in a way that the more $PTP is staked the higher the reward would be yielded as a proportion of the aggregate weights in the account, and the rewards takes 10 months to compile as mentioned. Therefore, the protocol that could accumulate the more amount of $PTP should have a head start against the another competitor.

Optically speaking, Vector is attracting $PTP users to stake on its platform by offering a higher % of the protocol’s revenue to stakers compared to Echidna. However, Echidna has responded by launching Echidna Rush that yields 4x rewards via conversion of $PTP to $ECD. Currently the platform already has a total of ~1.1mn $PTP deposited (as of the day of publication), while Vector only has ~800k $PTP. Not to mention a part of $PTP deposited to Vector would be used to provide liquidity for the xPTP-PTP pair on TraderJoe which might further reduces $PTP staked on Platypus Finance. That said, it is a caring move to platform supporters.

Another part of the equation is the deposit, the value locked in the account, which means there is something to do with the LP tokens. Echidna apparently designs its tokenomics in a way that rewards stablecoin depositors by giving them 80% of the reward in $PTP; while Vector already has not much to offer but its native tokens since it gives a majority of rewards to lure $PTP holders.

Currently Vector has ~107mn TVL and Echidna only has ~9.8mn across five different stablecoins. The massive difference in TVL is due to the fact that Vector offers its native token $VTX as reward while $ECD does not offer their native token to LP token holders. This creates short-term speculators giving liquidity to Vector for its token rewards, but not to Echidna.

However, when Echidna accumulates enough $PTP to make a difference in APY compared to Vector and $VTX loses value since the demand for realizing profit would lead to constant selling pressure, catching up TVL would not be a problem.

The way Echidna Finance designed its tokenomics showcased that the founding team has forward-looking vision and understands the priorities in winning the Platypus War; they also understand how to make up for the short-term nuance the tokenomics has created. I am currently slightly tilted to Echidna Finance, but it all depends on how the Echidna Rush would develop and how would the team continue to make up for $PTP holder on the rewards to accumulate $PTP.